When it comes to life cover, putting a policy in trust can be just as important as recommending the right product. It’s a powerful tool for advisers to help clients protect their loved ones while ensuring money goes where it’s meant to, quickly and tax-efficiently. But trust-related admin has traditionally added friction to an otherwise streamlined advice journey.

That’s why we’re introducing a new update on the Protection Platform: advisers can now access links to insurer trust forms directly on Protection Platform for seven participating insurers: Beagle Street, LV=, Royal London, Scottish Widows, The Exeter, Virgin Money and Vitality.

Here’s what you need to know:

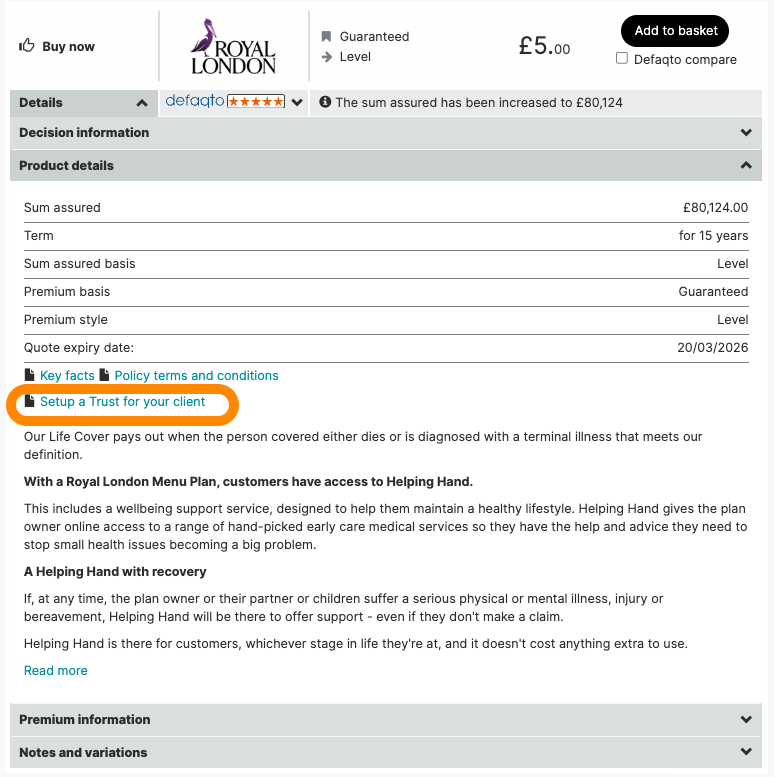

The links are located within the Product Details section on the Platform, pre and post submission.

LV= and Scottish Widows support fully digital trust setup via their extranets, whereas Royal London, The Exeter and Vitality offer digital submission by email.

We’ve created a handy Trust Forms FAQ & User Guide with links and step-by-step instructions to support you..

👉 Explore the Protection Platform

Why trusts matter

A trust is a legal arrangement that allows the proceeds from a life insurance policy to be paid directly to named beneficiaries — without forming part of the policyholder’s estate. This means the payout can avoid probate delays, potentially reduce inheritance tax liability, and be distributed in line with the policyholder’s wishes.

When a policy is written in trust:

The insurer pays the claim to the trustees (not the estate), enabling faster access to funds

It can help keep the proceeds outside the taxable estate

The policyholder retains control over who benefits from the payout, often with more precision than a will alone

The funds can be protected from certain risks, such as divorce or creditors, depending on how the trust is set up

Potential downsides to opting for a Trust

While putting a life insurance policy in trust offers clear advantages, it's not the right option for everyone. Advisers should help clients weigh up the potential trade-offs:

It’s (mostly) irreversible. Once a policy is written in trust, it’s considered a legal transfer of ownership — the client typically can’t pull it back or change their mind. That’s why it’s important the trust structure and beneficiaries are clearly thought through from the start.

Control shifts to the trustees. Once in trust, decisions about the policy — such as who benefits and when — must be made or approved by the appointed trustees. The policyholder can no longer act unilaterally.

Complexity in setup and admin. While trusts can provide long-term clarity, the initial setup can feel more complex for clients. Trustees must be chosen carefully, and advisers may need to support clients in understanding their obligations.

Why it matters for advisers

For advisers, positioning trusts is about helping clients achieve the outcome they actually intended — not just buying a product, but making sure it works for the people it’s meant to protect. This means ensuring clients are fully informed about both the benefits and the limitations of using a trust — helping them make a decision that aligns with their goals, circumstances, and comfort level.

Writing a policy in trust can materially improve client outcomes — faster payouts, lower tax exposure, and clearer control.

It shows deeper value beyond product recommendation — positioning the adviser as a holistic problem-solver.

It strengthens the adviser-client relationship by addressing what matters most to families in moments of loss.